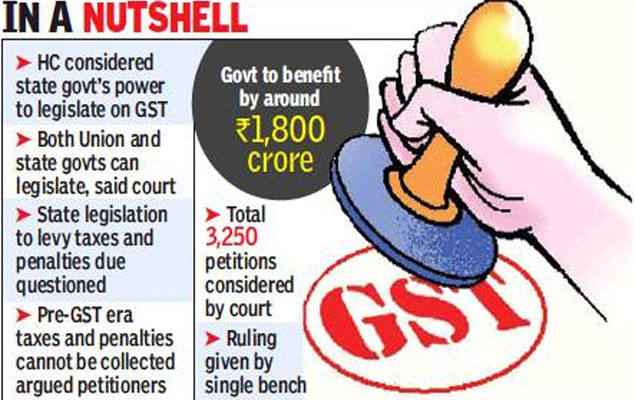

KOCHI: The high court, on Friday, dismissed a total of 3,250 petitions filed by business houses questioning the power of the state government to levy value-added tax and penalties for alleged tax evasion that occurred in years prior to the introduction of Goods and Services Tax (GST).

Justice Dama Seshadri Naidu ruled against the contention of the petitioners that the state government

lacked the power to add a Repeal and Saving provision (section 174) to Kerala State Goods and Services Act, 2017. Through the said provision, the government had specified that the change in law will not affect any tax, surcharge, penalty, or fine due.

Ruling that both the central and state governments have powers to legislate on GST, the court’s judgment said, “I am afraid it is a fallacy on the petitioners’ part to contend that the state lacks the legislative power to enact Section 174 of the KGST Act. Article 246A is the special provision on the Goods and Services Tax. It empowers, as rightly contended by Venkataraman, for the first time, both the Union and the state have been conferred simultaneous – not concurrent – powers to legislate on certain items. Indeed, concurrency yields to the doctrine of repugnancy, but simultaneous legislative power does not. That is, both the legislatures, say one from the Union and the other from the state, coexist-operate in the same sphere subject to other constitutional safeguards.”

In the petition (WP-C No. 11335/2018) that was considered as the lead case in the judgment, penalties imposed for 2010-11 and 2011-12 for alleged tax evasion after availing compounding rates of taxation were challenged.

The common argument of the petitioners was that state government has been denuded of its legislative power to enact Kerala State Goods and Services Act, 2017. As Kerala State GST Act came into being as a consequence to the constitutional amendment for GST, the provisions of other state legislations that existed earlier are no more valid, they had contended. The saving mechanism regarding transactions before September 16, 2017 crumbles, it was contended.

Justice Dama Seshadri Naidu ruled against the contention of the petitioners that the state government

lacked the power to add a Repeal and Saving provision (section 174) to Kerala State Goods and Services Act, 2017. Through the said provision, the government had specified that the change in law will not affect any tax, surcharge, penalty, or fine due.

Ruling that both the central and state governments have powers to legislate on GST, the court’s judgment said, “I am afraid it is a fallacy on the petitioners’ part to contend that the state lacks the legislative power to enact Section 174 of the KGST Act. Article 246A is the special provision on the Goods and Services Tax. It empowers, as rightly contended by Venkataraman, for the first time, both the Union and the state have been conferred simultaneous – not concurrent – powers to legislate on certain items. Indeed, concurrency yields to the doctrine of repugnancy, but simultaneous legislative power does not. That is, both the legislatures, say one from the Union and the other from the state, coexist-operate in the same sphere subject to other constitutional safeguards.”

In the petition (WP-C No. 11335/2018) that was considered as the lead case in the judgment, penalties imposed for 2010-11 and 2011-12 for alleged tax evasion after availing compounding rates of taxation were challenged.

The common argument of the petitioners was that state government has been denuded of its legislative power to enact Kerala State Goods and Services Act, 2017. As Kerala State GST Act came into being as a consequence to the constitutional amendment for GST, the provisions of other state legislations that existed earlier are no more valid, they had contended. The saving mechanism regarding transactions before September 16, 2017 crumbles, it was contended.

No comments:

Post a Comment