The Board has

clarified an issue in respect of transfer of input tax credit in case of

death of sole proprietor vide circular no. 96/15/2019-GST dated 28thMarch,

2019. There are so many doubts have been raised whether section 18(3)

of CGST Act provides for transfer of input tax credit which remains

unutilized to the transferee in case of death of the sole proprietor.

As

per Rule 41(1) of CGST Rules, the registered person i.e. (transferor of

business) can file FORM

GST ITC -02 electronically on the common portal

along with a request for transfer of unutilized input tax credit lying

in his electronic credit ledger to the transferee.

Further,

clarification has also been given in respect of procedure of filing of

FORM GST ITC-02 in case of death of the sole proprietor.

In

case of death of sole proprietor if the business is continued by any

person being transferee or successor, the input tax credit which remains

un-utilized in the electronic credit ledger is allowed to be

transferred to the transferee as per provisions and in the manner stated

below –

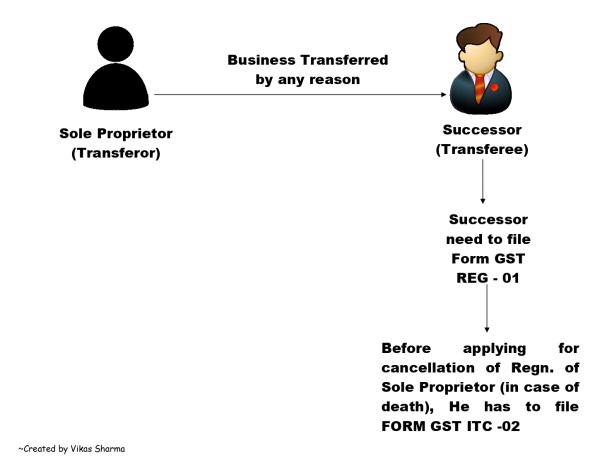

Registration liability of the transferee / successor: As

per section 22(3) of the CGST Act, the transferee or the successor

shall be liable to be registered with effect from the date of such

transfer or succession, where a business is transferred to another

person for any reasons including death of the proprietor. While filing

application in FORM GST REG-01 electronically in the common portal the

applicant is required to mention the reason to obtain registration as 'death of the proprietor'.

Cancellation of registration on account of death of the proprietor: Section

29(1)(a) of the CGST Act, allows the legal heirs in case of death of

sole proprietor of a business, to file application for cancellation of

registration in FORM GST REG-16 electronically on common portal on

account of transfer of business for any reason including death of the

proprietor. In FORM GST REG-16, reason for cancellation is required to

be mentioned as 'death of sole proprietor'. The GSTIN of

transferee to whom the business has been transferred is also required to

be mentioned to link the GSTIN of the transferor with the GSTIN of

transferee.

Transfer of input tax credit and liability: In

case of death of sole proprietor, if the business is continued by any

person being transferee or successor of business, it shall be construed

as transfer of business. Section 18(3) of the CGST Act, allows the

registered person to transfer the unutilized input tax credit lying in

his electronic credit ledger to the transferee in the manner prescribed

in rule 41 of the CGST Rules, where there is specific provision for

transfer of liabilities. As per Section 85(1) of the CGST Act, the

transferor and the transferee / successor shall jointly and severally be

liable to pay any tax, interest or any penalty due from the transferor

in cases of transfer of business 'in whole or in part, by sale, gift,

lease, leave and license, hire or in any other manner whatsoever'.

Furthermore,

Section 93(1) of the CGST Act provides that where a person, liable to

pay tax, interest or penalty under the CGST Act, dies, then the person

who continues business after his death, shall be liable to pay tax,

interest or penalty due from such person under this Act.

It

is therefore clarified that the transferee / successor shall be liable

to pay any tax, interest or any penalty due from the transferor in cases

of transfer of business due to death of sole proprietor.

Manner of transfer of credit: As

per rule 41(1) of the CGST Rules, a registered person shall file FORM

GST ITC-02 electronically on the common portal with a request for

transfer of unutilized input tax credit lying in his electronic credit

ledger to the transferee, in the event of sale, merger, de-merger,

amalgamation, lease or transfer or change in the ownership of business

for any reason.

In case of transfer of business on account of death of sole proprietor, thetransferee / successor shall

file FORM GST ITC-02 in respect of the registration which is required

to be cancelled on account of death of the sole proprietor. FORM GST

ITC-02 is required to be filed by the transferee/successor before filing

the application for cancellation of such registration. Upon acceptance

by the transferee / successor, the un-utilized input tax credit

specified in FORM GST ITC-02 shall be credited to his electronic credit

ledger.

No comments:

Post a Comment